Page 821 - ISC PROCEEDINGS 21.4

P. 821

3. Methodologies of research

3.1. Sampling and data acquisition

Utilising a synthesis of prior research, the authors created a preliminary survey

questionnaire and executed a pilot survey with 50 participants (n = 50) to assess the clarity

and appropriateness of the observed factors in the scale. The pilot survey results were

utilised to modify and enhance the official questionnaire prior to executing a large-scale

survey. The research employed a convenience sample strategy, targeting accounting

lecturers and third- and fourth-year accounting students at institutions. These entities are

directly engaged in the educational process and are thus equipped to assess the degree of

innovation in accounting pedagogy. The poll yielded 295 valid replies, which were utilised for

the subsequent analytical procedures.

3.2. Research methodology

The study employed a mixed-methods approach, integrating qualitative and

quantitative techniques. Qualitative research encompasses a literature review and analysis

of prior studies to ascertain elements that may affect teaching innovation in accounting

education, so establishing a foundation for presenting a model and research hypotheses.

Consequently, quantitative research was undertaken to evaluate the proposed model and

hypotheses. Data for the research was gathered via an online survey targeting accounting

lecturers and third- and fourth-year accounting students at institutions from December 2025

to January 2026. The survey instrument was constructed with a 5-point Likert scale. Prior to

administering the official survey, a pilot survey was executed including 50 lecturers and

professionals in accounting to evaluate and refine the questionnaire content. The official

survey produced 295 legitimate replies, which were utilised for data analysis. The data were

analysed using SPSS 26 software employing techniques like descriptive statistics, scale

reliability assessment, and regression analysis to evaluate the correlations among variables

in the research model.

4. Research findings

4.1. Evaluating the reliability of the scales

The reliability of the scales was assessed using Cronbach's Alpha coefficient. The

analytical results indicated that the majority of the observed variables satisfied the criteria

(Cronbach's Alpha coefficient ≥ 0.6 and item-total correlation coefficient ≥ 0.3). Following

Cronbach's Alpha assessment, the study model kept 6 independent variables and 1

dependent variable, including 22 observed variables, for exploratory factor analysis (EFA).

The independent variables were analysed concurrently, whilst the dependent variable

"Innovation in accounting teaching methods" was examined independently. The

independent variable values were evaluated using fundamental statistical techniques,

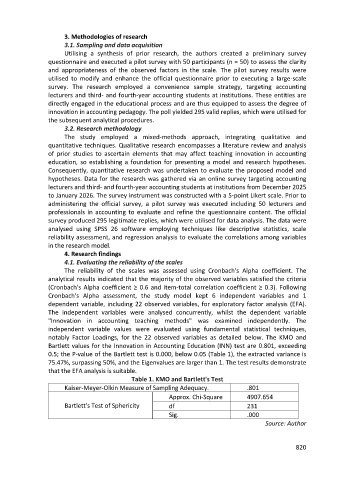

notably Factor Loadings, for the 22 observed variables as detailed below. The KMO and

Bartlett values for the Innovation in Accounting Education (INN) test are 0.801, exceeding

0.5; the P-value of the Bartlett test is 0.000, below 0.05 (Table 1), the extracted variance is

75.47%, surpassing 50%, and the Eigenvalues are larger than 1. The test results demonstrate

that the EFA analysis is suitable.

Table 1. KMO and Bartlett's Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy. .801

Approx. Chi-Square 4907.654

Bartlett's Test of Sphericity df 231

Sig. .000

Source: Author

820