Page 820 - ISC PROCEEDINGS 21.4

P. 820

course imparts specialised knowledge while cultivating abilities in accounting software,

information systems, and data analysis. Incorporating technology into curricula is thought to

foster innovation in pedagogical approaches, broaden flexible learning modalities, and

improve involvement with professional practice (Bond et al., 2018; OECD, 2025; Redecker,

2017). Consequently, the research posits the hypothesis:

H3: Digital-oriented curriculum enhances pedagogical innovation.

Organizational support

Barney's (1991) perspective posits that school rules and resources will foster an

environment conducive to lecturers implementing innovative teaching methods and

incorporating technology into the educational process. This support is evidenced by policies

that promote innovation in pedagogical approaches, facilitate curricula to augment

lecturers' technical proficiency, and allocate funding for instructional activities. The study

posits the hypothesis:

H4: Organizational support enhances pedagogical innovation

Collaboration with enterprises

This is seen as a significant factor in fostering educational innovation in higher

education. This collaboration enables training institutions to align the curriculum with the

actual demands of the labour market by engaging in curriculum creation, facilitating

internships, and exchanging professional expertise from enterprises. In accounting

education, corporate engagement facilitates the enhancement of processes, technologies,

and professional competencies, consequently fostering innovation in content and

pedagogical approaches to elevate training quality (OECD, 2025). The study posits the

hypothesis:

H5: Collaboration with enterprises in accounting education enhances pedagogical

innovation.

Application of digital technology

The utilisation of online learning platforms, learning management systems (LMS),

accounting software, and digital technologies improves engagement, broadens flexible

learning modalities, and aids learners in acquiring knowledge more efficiently. In accounting

education, the incorporation of digital technologies into instructional activities enhances the

linkage between theoretical concepts and professional practice, hence elevating the quality

of training within the digital economy (Davis, 1989; OECD, 2025). The study posits the

hypothesis:

H6: The extent of Application of Digital Technology in accounting education favourably

impacts pedagogical innovation.

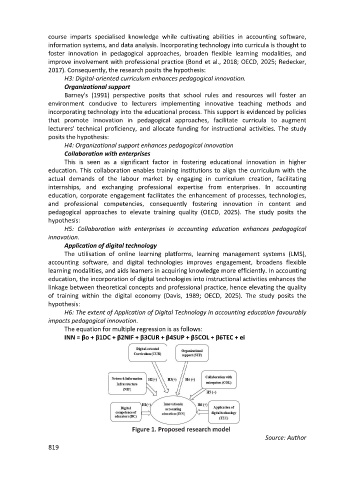

The equation for multiple regression is as follows:

INN = βo + β1DC + β2NIF + β3CUR + β4SUP + β5COL + β6TEC + ei

Figure 1. Proposed research model

Source: Author

819