Page 192 - ISC PROCEEDINGS 21.4

P. 192

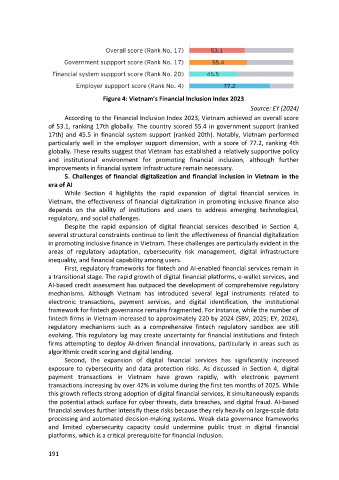

Figure 4: Vietnam’s Financial Inclusion Index 2023

Source: EY (2024)

According to the Financial Inclusion Index 2023, Vietnam achieved an overall score

of 53.1, ranking 17th globally. The country scored 55.4 in government support (ranked

17th) and 45.5 in financial system support (ranked 20th). Notably, Vietnam performed

particularly well in the employer support dimension, with a score of 77.2, ranking 4th

globally. These results suggest that Vietnam has established a relatively supportive policy

and institutional environment for promoting financial inclusion, although further

improvements in financial system infrastructure remain necessary.

5. Challenges of financial digitalization and financial inclusion in Vietnam in the

era of AI

While Section 4 highlights the rapid expansion of digital financial services in

Vietnam, the effectiveness of financial digitalization in promoting inclusive finance also

depends on the ability of institutions and users to address emerging technological,

regulatory, and social challenges.

Despite the rapid expansion of digital financial services described in Section 4,

several structural constraints continue to limit the effectiveness of financial digitalization

in promoting inclusive finance in Vietnam. These challenges are particularly evident in the

areas of regulatory adaptation, cybersecurity risk management, digital infrastructure

inequality, and financial capability among users.

First, regulatory frameworks for fintech and AI-enabled financial services remain in

a transitional stage. The rapid growth of digital financial platforms, e-wallet services, and

AI-based credit assessment has outpaced the development of comprehensive regulatory

mechanisms. Although Vietnam has introduced several legal instruments related to

electronic transactions, payment services, and digital identification, the institutional

framework for fintech governance remains fragmented. For instance, while the number of

fintech firms in Vietnam increased to approximately 220 by 2024 (SBV, 2025; EY, 2024),

regulatory mechanisms such as a comprehensive fintech regulatory sandbox are still

evolving. This regulatory lag may create uncertainty for financial institutions and fintech

firms attempting to deploy AI-driven financial innovations, particularly in areas such as

algorithmic credit scoring and digital lending.

Second, the expansion of digital financial services has significantly increased

exposure to cybersecurity and data protection risks. As discussed in Section 4, digital

payment transactions in Vietnam have grown rapidly, with electronic payment

transactions increasing by over 42% in volume during the first ten months of 2025. While

this growth reflects strong adoption of digital financial services, it simultaneously expands

the potential attack surface for cyber threats, data breaches, and digital fraud. AI-based

financial services further intensify these risks because they rely heavily on large-scale data

processing and automated decision-making systems. Weak data governance frameworks

and limited cybersecurity capacity could undermine public trust in digital financial

platforms, which is a critical prerequisite for financial inclusion.

191