Page 392 - Ebook HTKH 2024

P. 392

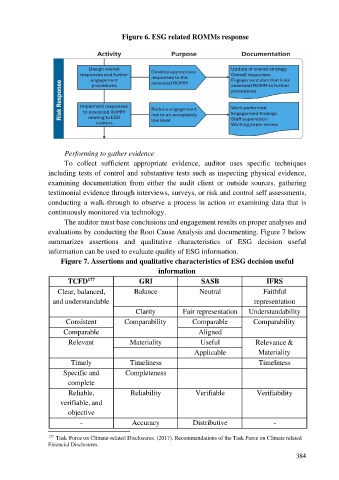

Figure 6. ESG related ROMMs response

Performing to gather evidence

To collect sufficient appropriate evidence, auditor uses specific techniques

including tests of control and substantive tests such as inspecting physical evidence,

examining documentation from either the audit client or outside sources, gathering

testimonial evidence through interviews, surveys, or risk and control self assessments,

conducting a walk-through to observe a process in action or examining data that is

continuously monitored via technology.

The auditor must base conclusions and engagement results on proper analyses and

evaluations by conducting the Root Cause Analysis and documenting. Figure 7 below

summarizes assertions and qualitative characteristics of ESG decision useful

information can be used to evaluate quality of ESG information.

Figure 7. Assertions and qualitative characteristics of ESG decision useful

information

177

TCFD GRI SASB IFRS

Clear, balanced, Balance Neutral Faithful

and understandable representation

Clarity Fair representation Understandability

Consistent Comparability Comparable Comparability

Comparable Aligned

Relevant Materiality Useful Relevance &

Applicable Materiality

Timely Timeliness Timeliness

Specific and Completeness

complete

Reliable, Reliability Verifiable Verifiability

verifiable, and

objective

- Accuracy Distributive -

177 Task Force on Climate-related Disclosures. (2017). Recommendations of the Task Force on Climate related

Financial Disclosures.

384