Page 390 - Ebook HTKH 2024

P. 390

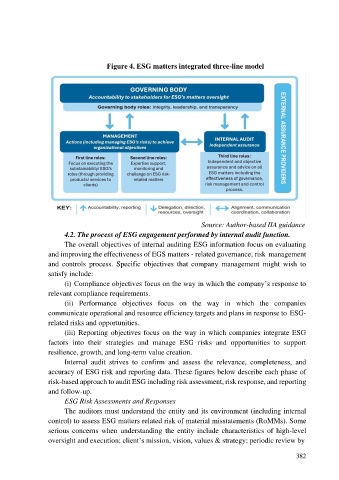

Figure 4. ESG matters integrated three-line model

Source: Author-based IIA guidance

4.2. The process of ESG engagement performed by internal audit function.

The overall objectives of internal auditing ESG information focus on evaluating

and improving the effectiveness of EGS matters - related governance, risk management

and controls process. Specific objectives that company management might wish to

satisfy include:

(i) Compliance objectives focus on the way in which the company’s response to

relevant compliance requirements.

(ii) Performance objectives focus on the way in which the companies

communicate operational and resource efficiency targets and plans in response to ESG-

related risks and opportunities.

(iii) Reporting objectives focus on the way in which companies integrate ESG

factors into their strategies and manage ESG risks and opportunities to support

resilience, growth, and long-term value creation.

Internal audit strives to confirm and assess the relevance, completeness, and

accuracy of ESG risk and reporting data. These figures below describe each phase of

risk-based approach to audit ESG including risk assessment, risk response, and reporting

and follow-up.

ESG Risk Assessments and Responses

The auditors must understand the entity and its environment (including internal

control) to assess ESG matters related risk of material misstatements (RoMMs). Some

serious concerns when understanding the entity include characteristics of high-level

oversight and execution; client’s mission, vision, values & strategy; periodic review by

382