Page 374 - Ebook HTKH 2024

P. 374

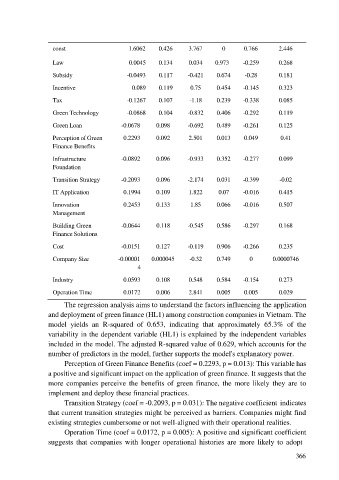

const 1.6062 0.426 3.767 0 0.766 2.446

Law 0.0045 0.134 0.034 0.973 -0.259 0.268

Subsidy -0.0493 0.117 -0.421 0.674 -0.28 0.181

Incentive 0.089 0.119 0.75 0.454 -0.145 0.323

Tax -0.1267 0.107 -1.18 0.239 -0.338 0.085

Green Technology -0.0868 0.104 -0.832 0.406 -0.292 0.119

Green Loan -0.0678 0.098 -0.692 0.489 -0.261 0.125

Perception of Green 0.2293 0.092 2.501 0.013 0.049 0.41

Finance Benefits

Infrastructure -0.0892 0.096 -0.933 0.352 -0.277 0.099

Foundation

Transition Strategy -0.2093 0.096 -2.174 0.031 -0.399 -0.02

IT Application 0.1994 0.109 1.822 0.07 -0.016 0.415

Innovation 0.2453 0.133 1.85 0.066 -0.016 0.507

Management

Building Green -0.0644 0.118 -0.545 0.586 -0.297 0.168

Finance Solutions

Cost -0.0151 0.127 -0.119 0.906 -0.266 0.235

Company Size -0.00001 0.000045 -0.32 0.749 0 0.0000746

4

Industry 0.0593 0.108 0.548 0.584 -0.154 0.273

Operation Time 0.0172 0.006 2.841 0.005 0.005 0.029

The regression analysis aims to understand the factors influencing the application

and deployment of green finance (HL1) among construction companies in Vietnam. The

model yields an R-squared of 0.653, indicating that approximately 65.3% of the

variability in the dependent variable (HL1) is explained by the independent variables

included in the model. The adjusted R-squared value of 0.629, which accounts for the

number of predictors in the model, further supports the model's explanatory power.

Perception of Green Finance Benefits (coef = 0.2293, p = 0.013): This variable has

a positive and significant impact on the application of green finance. It suggests that the

more companies perceive the benefits of green finance, the more likely they are to

implement and deploy these financial practices.

Transition Strategy (coef = -0.2093, p = 0.031): The negative coefficient indicates

that current transition strategies might be perceived as barriers. Companies might find

existing strategies cumbersome or not well-aligned with their operational realities.

Operation Time (coef = 0.0172, p = 0.005): A positive and significant coefficient

suggests that companies with longer operational histories are more likely to adopt

366