Page 519 - ISC PROCEEDINGS 21.4

P. 519

Note: ***, **, and * indicate the significance at the 1%, 5%, and 10% level,

respectively.

Source: Authors’ compilation from analysis data with Stata 17

The table above presents the Fixed Effects regression results with clustered

standard errors for bank stability (LN1ZSCORE). ESG is positively and significantly

associated with bank stability (β = 0.2034, p < 0.01), supporting H1. CORRUPTION also

shows a positive and significant coefficient (β = 0.0312, p < 0.01), consistent with H2. By

contrast, LN_TA, EA, and GDPG are not statistically significant. EFFR is negatively

associated with bank stability at the 1% level, while inflation is positive and significant at

the same level. These results should be interpreted as statistical associations rather than

causal effects.

The within R-squared of 0.2722 indicates that the explanatory variables account for

a meaningful share of within-bank variation in bank stability over time. The rho value of

0.6371 suggests that a substantial proportion of the total variance is attributable to

unobserved bank-specific effects. Clustering standard errors at the bank level further

improves inference by accounting for heteroskedasticity and within-bank serial

correlation.

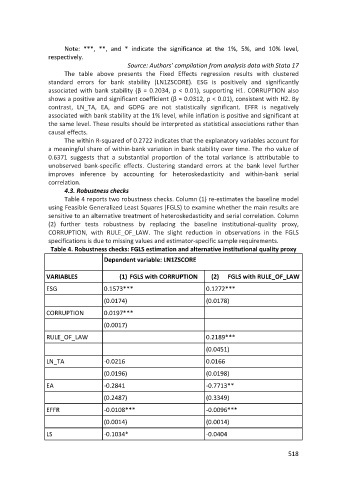

4.3. Robustness checks

Table 4 reports two robustness checks. Column (1) re-estimates the baseline model

using Feasible Generalized Least Squares (FGLS) to examine whether the main results are

sensitive to an alternative treatment of heteroskedasticity and serial correlation. Column

(2) further tests robustness by replacing the baseline institutional-quality proxy,

CORRUPTION, with RULE_OF_LAW. The slight reduction in observations in the FGLS

specifications is due to missing values and estimator-specific sample requirements.

Table 4. Robustness checks: FGLS estimation and alternative institutional quality proxy

Dependent variable: LN1ZSCORE

VARIABLES (1) FGLS with CORRUPTION (2) FGLS with RULE_OF_LAW

ESG 0.1573*** 0.1272***

(0.0174) (0.0178)

CORRUPTION 0.0197***

(0.0017)

RULE_OF_LAW 0.2189***

(0.0451)

LN_TA -0.0216 0.0166

(0.0196) (0.0198)

EA -0.2841 -0.7713**

(0.2487) (0.3349)

EFFR -0.0108*** -0.0096***

(0.0014) (0.0014)

LS -0.1034* -0.0404

518