Page 516 - ISC PROCEEDINGS 21.4

P. 516

ESGit captures ESG performance

CORRUPTIONct represents country-level corruption

LN_TA, EA, EFFR, and LS denote bank size, capital adequacy, efficiency ratio, and

liability structure respectively

GDPG and INFLATION are macroeconomic controls

μᵢ captures bank-specific effects

λₜ captures time fixed effects

εᵢₜ is the idiosyncratic error term

This specification allows the analysis to estimate the relationship between ESG

performance and bank stability while controlling for bank-level characteristics and

macroeconomic conditions.

3.3. Regression methods

To ensure the reliability of the empirical findings, the study employs a sequence of

panel data estimators. The analysis begins with Pooled OLS as a baseline specification,

followed by Random Effects (RE) and Fixed Effects (FE) models to account for unobserved

bank-specific heterogeneity. An F-test confirms the presence of individual effects, while

the Hausman test indicates that the FE model is preferred, suggesting that unobserved

bank characteristics are correlated with the explanatory variables.

Subsequent diagnostic tests reveal the presence of heteroskedasticity and serial

correlation within panels. To address these issues, the primary specification adopts a

Fixed Effects model with standard errors clustered at the bank level, which provides

robust inference under both heteroskedasticity and within-bank autocorrelation. As an

additional robustness check, the Feasible Generalized Least Squares (FGLS) estimator is

applied to explicitly model cross-sectional heteroskedasticity and serial dependence. The

consistency of results across FE-clustered and FGLS estimations reinforces the robustness

and credibility of the baseline findings.

4. Empirical results and discussion

4.1. Descriptive statistics & correlation

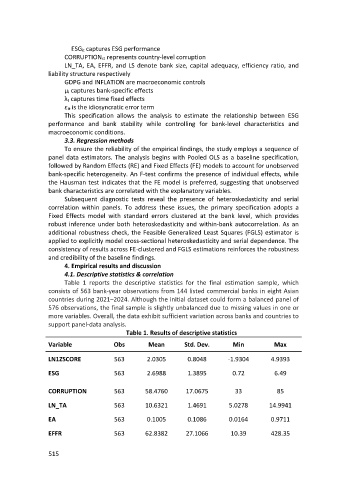

Table 1 reports the descriptive statistics for the final estimation sample, which

consists of 563 bank-year observations from 144 listed commercial banks in eight Asian

countries during 2021–2024. Although the initial dataset could form a balanced panel of

576 observations, the final sample is slightly unbalanced due to missing values in one or

more variables. Overall, the data exhibit sufficient variation across banks and countries to

support panel-data analysis.

Table 1. Results of descriptive statistics

Variable Obs Mean Std. Dev. Min Max

LN1ZSCORE 563 2.0305 0.8048 -1.9304 4.9393

ESG 563 2.6988 1.3895 0.72 6.49

CORRUPTION 563 58.4760 17.0675 33 85

LN_TA 563 10.6321 1.4691 5.0278 14.9941

EA 563 0.1005 0.1086 0.0164 0.9711

EFFR 563 62.8382 27.1066 10.39 428.35

515