Page 497 - ISC PROCEEDINGS 21.4

P. 497

standardizing years of historical data. Furthermore, banks must navigate the delicate

balance between leveraging data for AI training and complying with stringent personal

data protection regulations.

Shortage of High-Quality AI Talent: The Vietnamese market is experiencing a severe

deficit of professionals capable of bridging the gap between financial expertise and AI

technology. Commercial banks are not only competing with one another but are also

locked in a 'war for talent' against Big Tech giants (such as Google, Grab, and Shopee) to

attract top-tier Data Scientists. Simultaneously, traditional banking staff face immense

pressure to undergo reskilling to operate alongside automated systems, leading to a

heightened risk of personnel turnover.

Black Box' Risks and Transparency: The lack of interpretability in AI models poses a

significant risk; if a loan is rejected, banks struggle to provide a detailed 'why' to

customers or regulators, which undermines transparency in the financial sector.

Furthermore, if training data contains inherent algorithmic bias—such as historical

defaults concentrated in specific regions—AI may inadvertently 'learn' and perpetuate

discriminatory practices against those demographics in the future.

Legacy Infrastructure Barriers: A majority of Vietnamese banks still operate on

legacy Core Banking platforms, making it exceptionally difficult to integrate modern AI

applications that require real-time processing into bulky, monolithic systems. The

financial burden of migrating infrastructure from on-premise servers to the cloud to

support AI is a substantial hurdle, particularly for mid-sized institutions.

Regulatory Vacuum and Cybercrime: There is currently no comprehensive legal

framework to assign liability when AI causes errors or financial losses for customers.

While banks deploy AI for security, cybercriminals are simultaneously utilizing AI to create

Deepfakes (facial and voice spoofing) to bypass eKYC layers, exerting constant defensive

pressure on financial institutions.

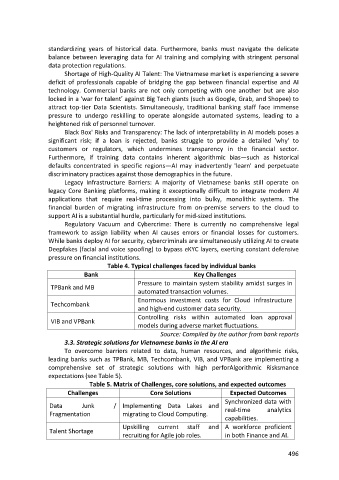

Table 4. Typical challenges faced by individual banks

Bank Key Challenges

Pressure to maintain system stability amidst surges in

TPBank and MB

automated transaction volumes.

Enormous investment costs for Cloud infrastructure

Techcombank

and high-end customer data security.

Controlling risks within automated loan approval

VIB and VPBank

models during adverse market fluctuations.

Source: Compiled by the author from bank reports

3.3. Strategic solutions for Vietnamese banks in the AI era

To overcome barriers related to data, human resources, and algorithmic risks,

leading banks such as TPBank, MB, Techcombank, VIB, and VPBank are implementing a

comprehensive set of strategic solutions with high perforAlgorithmic Risksmance

expectations (see Table 5).

Table 5. Matrix of Challenges, core solutions, and expected outcomes

Challenges Core Solutions Expected Outcomes

Synchronized data with

Data Junk / Implementing Data Lakes and real-time analytics

Fragmentation migrating to Cloud Computing.

capabilities.

Upskilling current staff and A workforce proficient

Talent Shortage

recruiting for Agile job roles. in both Finance and AI.

496