Page 498 - ISC PROCEEDINGS 21.4

P. 498

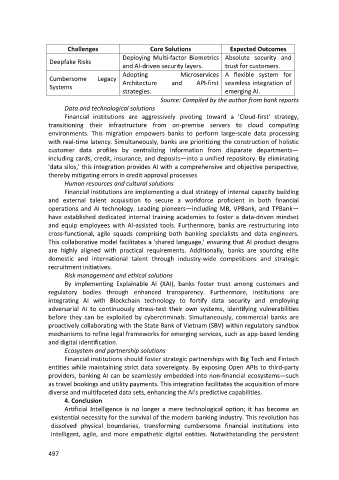

Challenges Core Solutions Expected Outcomes

Deploying Multi-factor Biometrics Absolute security and

Deepfake Risks

and AI-driven security layers. trust for customers.

Adopting Microservices A flexible system for

Cumbersome Legacy Architecture and API-first seamless integration of

Systems

strategies. emerging AI.

Source: Compiled by the author from bank reports

Data and technological solutions

Financial institutions are aggressively pivoting toward a 'Cloud-first' strategy,

transitioning their infrastructure from on-premise servers to cloud computing

environments. This migration empowers banks to perform large-scale data processing

with real-time latency. Simultaneously, banks are prioritizing the construction of holistic

customer data profiles by centralizing information from disparate departments—

including cards, credit, insurance, and deposits—into a unified repository. By eliminating

'data silos,' this integration provides AI with a comprehensive and objective perspective,

thereby mitigating errors in credit approval processes

Human resources and cultural solutions

Financial institutions are implementing a dual strategy of internal capacity building

and external talent acquisition to secure a workforce proficient in both financial

operations and AI technology. Leading pioneers—including MB, VPBank, and TPBank—

have established dedicated internal training academies to foster a data-driven mindset

and equip employees with AI-assisted tools. Furthermore, banks are restructuring into

cross-functional, agile squads comprising both banking specialists and data engineers.

This collaborative model facilitates a 'shared language,' ensuring that AI product designs

are highly aligned with practical requirements. Additionally, banks are sourcing elite

domestic and international talent through industry-wide competitions and strategic

recruitment initiatives.

Risk management and ethical solutions

By implementing Explainable AI (XAI), banks foster trust among customers and

regulatory bodies through enhanced transparency. Furthermore, institutions are

integrating AI with Blockchain technology to fortify data security and employing

adversarial AI to continuously stress-test their own systems, identifying vulnerabilities

before they can be exploited by cybercriminals. Simultaneously, commercial banks are

proactively collaborating with the State Bank of Vietnam (SBV) within regulatory sandbox

mechanisms to refine legal frameworks for emerging services, such as app-based lending

and digital identification.

Ecosystem and partnership solutions

Financial institutions should foster strategic partnerships with Big Tech and Fintech

entities while maintaining strict data sovereignty. By exposing Open APIs to third-party

providers, banking AI can be seamlessly embedded into non-financial ecosystems—such

as travel bookings and utility payments. This integration facilitates the acquisition of more

diverse and multifaceted data sets, enhancing the AI's predictive capabilities.

4. Conclusion

Artificial Intelligence is no longer a mere technological option; it has become an

existential necessity for the survival of the modern banking industry. This revolution has

dissolved physical boundaries, transforming cumbersome financial institutions into

intelligent, agile, and more empathetic digital entities. Notwithstanding the persistent

497