Page 493 - ISC PROCEEDINGS 21.4

P. 493

Transitioning to AI is not merely about installing software; it is a fundamental

transformation of the entire operational machinery onto a new technological foundation.

Legacy System Constraints: Traditional core banking systems often lack the flexibility

required to integrate with AI applications, which demand massive real-time data

processing capabilities. Specialist Shortages: There is a significant market deficit of

professionals who possess deep expertise in both finance and data science. Meanwhile,

traditional staff face the mounting pressure of displacement unless they undergo

comprehensive retraining.

Concentration and legal risks

Dependence on Third-Party AI Providers: Most banks currently lease AI

infrastructure from tech giants (Google, Microsoft, Amazon). If these partners experience

technical failures or outages, the global financial system could face simultaneous paralysis.

Incomplete Legal Frameworks: In Vietnam and many other nations, specific

regulations regarding legal liability when AI causes errors (e.g., resulting in the loss of

customer funds) are still under development. This creates a "gray zone" of risk for

banking institutions.

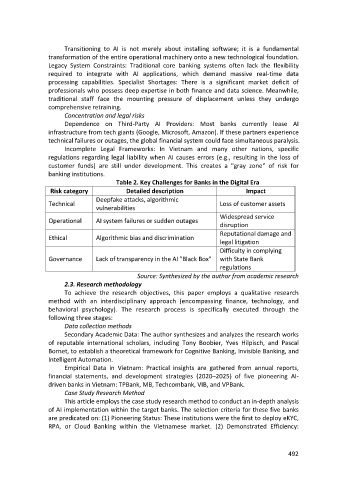

Table 2. Key Challenges for Banks in the Digital Era

Risk category Detailed description Impact

Deepfake attacks, algorithmic

Technical Loss of customer assets

vulnerabilities

Widespread service

Operational AI system failures or sudden outages

disruption

Reputational damage and

Ethical Algorithmic bias and discrimination

legal litigation

Difficulty in complying

Governance Lack of transparency in the AI "Black Box" with State Bank

regulations

Source: Synthesized by the author from academic research

2.3. Research methodology

To achieve the research objectives, this paper employs a qualitative research

method with an interdisciplinary approach (encompassing finance, technology, and

behavioral psychology). The research process is specifically executed through the

following three stages:

Data collection methods

Secondary Academic Data: The author synthesizes and analyzes the research works

of reputable international scholars, including Tony Boobier, Yves Hilpisch, and Pascal

Bornet, to establish a theoretical framework for Cognitive Banking, Invisible Banking, and

Intelligent Automation.

Empirical Data in Vietnam: Practical insights are gathered from annual reports,

financial statements, and development strategies (2020–2025) of five pioneering AI-

driven banks in Vietnam: TPBank, MB, Techcombank, VIB, and VPBank.

Case Study Research Method

This article employs the case study research method to conduct an in-depth analysis

of AI implementation within the target banks. The selection criteria for these five banks

are predicated on: (1) Pioneering Status: These institutions were the first to deploy eKYC,

RPA, or Cloud Banking within the Vietnamese market. (2) Demonstrated Efficiency:

492