Page 492 - ISC PROCEEDINGS 21.4

P. 492

gold) based on each individual's financial goals and risk tolerance. Furthermore, by

collecting and processing data from economic news, global financial reports, and industry

or corporate financial statements, AI generates high-precision short-term forecasts for

exchange rates, interest rates, and stock markets. These insights serve as a reliable

reference for both customers and banks in their decision-making processes.

Open Banking and Ecosystems

AI acts as the catalyst, connecting banking operational platforms more effectively

than traditional banking methods. Embedded Finance, Banks provide intelligent APIs to

integrate lending and installment services directly into shopping, ride-hailing, and travel

applications. Cross-Data Analysis, AI analyzes data from partners within the ecosystem to

understand the holistic "big picture" of a customer's life, thereby offering the most

precise insurance packages or consumer incentives.

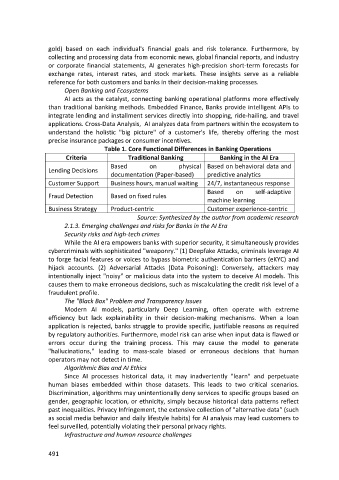

Table 1. Core Functional Differences in Banking Operations

Criteria Traditional Banking Banking in the AI Era

Based on physical Based on behavioral data and

Lending Decisions

documentation (Paper-based) predictive analytics

Customer Support Business hours, manual waiting 24/7, instantaneous response

Based on self-adaptive

Fraud Detection Based on fixed rules

machine learning

Business Strategy Product-centric Customer experience-centric

Source: Synthesized by the author from academic research

2.1.3. Emerging challenges and risks for Banks in the AI Era

Security risks and high-tech crimes

While the AI era empowers banks with superior security, it simultaneously provides

cybercriminals with sophisticated "weaponry." (1) Deepfake Attacks, criminals leverage AI

to forge facial features or voices to bypass biometric authentication barriers (eKYC) and

hijack accounts. (2) Adversarial Attacks (Data Poisoning): Conversely, attackers may

intentionally inject "noisy" or malicious data into the system to deceive AI models. This

causes them to make erroneous decisions, such as miscalculating the credit risk level of a

fraudulent profile.

The "Black Box" Problem and Transparency Issues

Modern AI models, particularly Deep Learning, often operate with extreme

efficiency but lack explainability in their decision-making mechanisms. When a loan

application is rejected, banks struggle to provide specific, justifiable reasons as required

by regulatory authorities. Furthermore, model risk can arise when input data is flawed or

errors occur during the training process. This may cause the model to generate

"hallucinations," leading to mass-scale biased or erroneous decisions that human

operators may not detect in time.

Algorithmic Bias and AI Ethics

Since AI processes historical data, it may inadvertently "learn" and perpetuate

human biases embedded within those datasets. This leads to two critical scenarios.

Discrimination, algorithms may unintentionally deny services to specific groups based on

gender, geographic location, or ethnicity, simply because historical data patterns reflect

past inequalities. Privacy Infringement, the extensive collection of "alternative data" (such

as social media behavior and daily lifestyle habits) for AI analysis may lead customers to

feel surveilled, potentially violating their personal privacy rights.

Infrastructure and human resource challenges

491