Page 557 - ISC PROCEEDINGS 21.4

P. 557

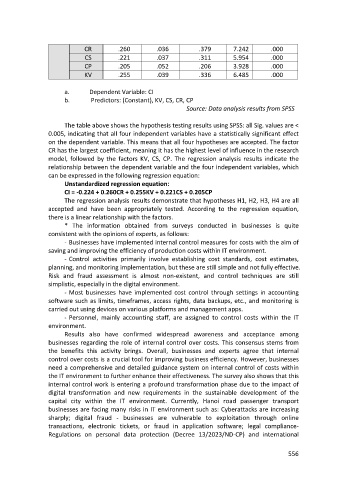

CR .260 .036 .379 7.242 .000

CS .221 .037 .311 5.954 .000

CP .205 .052 .206 3.928 .000

KV .255 .039 .336 6.485 .000

a. Dependent Variable: CI

b. Predictors: (Constant), KV, CS, CR, CP

Source: Data analysis results from SPSS

The table above shows the hypothesis testing results using SPSS: all Sig. values are <

0.005, indicating that all four independent variables have a statistically significant effect

on the dependent variable. This means that all four hypotheses are accepted. The factor

CR has the largest coefficient, meaning it has the highest level of influence in the research

model, followed by the factors KV, CS, CP. The regression analysis results indicate the

relationship between the dependent variable and the four independent variables, which

can be expressed in the following regression equation:

Unstandardized regression equation:

CI = -0.224 + 0.260CR + 0.255KV + 0.221CS + 0.205CP

The regression analysis results demonstrate that hypotheses H1, H2, H3, H4 are all

accepted and have been appropriately tested. According to the regression equation,

there is a linear relationship with the factors.

* The information obtained from surveys conducted in businesses is quite

consistent with the opinions of experts, as follows:

- Businesses have implemented internal control measures for costs with the aim of

saving and improving the efficiency of production costs within IT environment.

- Control activities primarily involve establishing cost standards, cost estimates,

planning, and monitoring implementation, but these are still simple and not fully effective.

Risk and fraud assessment is almost non-existent, and control techniques are still

simplistic, especially in the digital environment.

- Most businesses have implemented cost control through settings in accounting

software such as limits, timeframes, access rights, data backups, etc., and monitoring is

carried out using devices on various platforms and management apps.

- Personnel, mainly accounting staff, are assigned to control costs within the IT

environment.

Results also have confirmed widespread awareness and acceptance among

businesses regarding the role of internal control over costs. This consensus stems from

the benefits this activity brings. Overall, businesses and experts agree that internal

control over costs is a crucial tool for improving business efficiency. However, businesses

need a comprehensive and detailed guidance system on internal control of costs within

the IT environment to further enhance their effectiveness. The survey also shows that this

internal control work is entering a profound transformation phase due to the impact of

digital transformation and new requirements in the sustainable development of the

capital city within the IT environment. Currently, Hanoi road passenger transport

businesses are facing many risks in IT environment such as: Cyberattacks are increasing

sharply; digital fraud - businesses are vulnerable to exploitation through online

transactions, electronic tickets, or fraud in application software; legal compliance-

Regulations on personal data protection (Decree 13/2023/ND-CP) and international

556