Page 550 - ISC PROCEEDINGS 21.4

P. 550

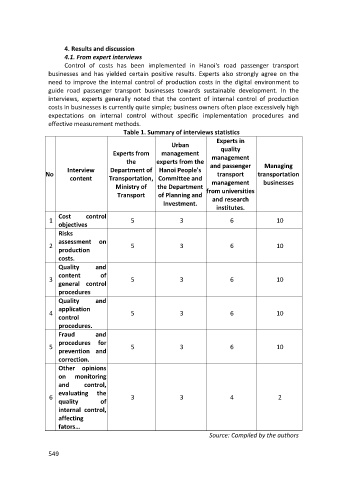

4. Results and discussion

4.1. From expert interviews

Control of costs has been implemented in Hanoi's road passenger transport

businesses and has yielded certain positive results. Experts also strongly agree on the

need to improve the internal control of production costs in the digital environment to

guide road passenger transport businesses towards sustainable development. In the

interviews, experts generally noted that the content of internal control of production

costs in businesses is currently quite simple; business owners often place excessively high

expectations on internal control without specific implementation procedures and

effective measurement methods.

Table 1. Summary of interviews statistics

Experts in

Urban

Experts from management quality

management

the experts from the and passenger Managing

Interview Department of Hanoi People's

No transport transportation

content Transportation, Committee and businesses

management

Ministry of the Department from universities

Transport of Planning and

Investment. and research

institutes.

Cost control

1 5 3 6 10

objectives

Risks

assessment on

2 5 3 6 10

production

costs.

Quality and

content of

3 5 3 6 10

general control

procedures

Quality and

application

4 5 3 6 10

control

procedures.

Fraud and

procedures for

5 5 3 6 10

prevention and

correction.

Other opinions

on monitoring

and control,

evaluating the

6 3 3 4 2

quality of

internal control,

affecting

fators…

Source: Compiled by the authors

549