Page 508 - ISC PROCEEDINGS 21.4

P. 508

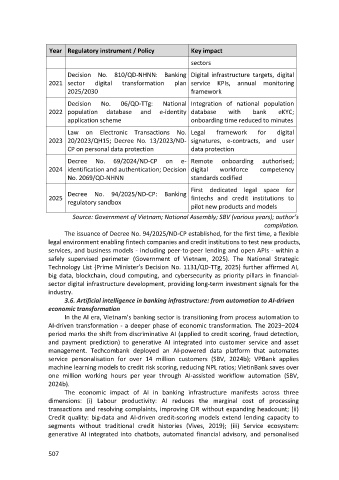

Year Regulatory instrument / Policy Key impact

sectors

Decision No. 810/QD-NHNN: Banking Digital infrastructure targets, digital

2021 sector digital transformation plan service KPIs, annual monitoring

2025/2030 framework

Decision No. 06/QD-TTg: National Integration of national population

2022 population database and e-identity database with bank eKYC;

application scheme onboarding time reduced to minutes

Law on Electronic Transactions No. Legal framework for digital

2023 20/2023/QH15; Decree No. 13/2023/ND- signatures, e-contracts, and user

CP on personal data protection data protection

Decree No. 69/2024/ND-CP on e- Remote onboarding authorised;

2024 identification and authentication; Decision digital workforce competency

No. 2069/QD-NHNN standards codified

First dedicated legal space for

Decree No. 94/2025/ND-CP: Banking

2025 fintechs and credit institutions to

regulatory sandbox

pilot new products and models

Source: Government of Vietnam; National Assembly; SBV (various years); author’s

compilation.

The issuance of Decree No. 94/2025/ND-CP established, for the first time, a flexible

legal environment enabling fintech companies and credit institutions to test new products,

services, and business models - including peer-to-peer lending and open APIs - within a

safely supervised perimeter (Government of Vietnam, 2025). The National Strategic

Technology List (Prime Minister’s Decision No. 1131/QD-TTg, 2025) further affirmed AI,

big data, blockchain, cloud computing, and cybersecurity as priority pillars in financial-

sector digital infrastructure development, providing long-term investment signals for the

industry.

3.6. Artificial intelligence in banking infrastructure: from automation to AI-driven

economic transformation

In the AI era, Vietnam’s banking sector is transitioning from process automation to

AI-driven transformation - a deeper phase of economic transformation. The 2023–2024

period marks the shift from discriminative AI (applied to credit scoring, fraud detection,

and payment prediction) to generative AI integrated into customer service and asset

management. Techcombank deployed an AI-powered data platform that automates

service personalisation for over 14 million customers (SBV, 2024b); VPBank applies

machine learning models to credit risk scoring, reducing NPL ratios; VietinBank saves over

one million working hours per year through AI-assisted workflow automation (SBV,

2024b).

The economic impact of AI in banking infrastructure manifests across three

dimensions: (i) Labour productivity: AI reduces the marginal cost of processing

transactions and resolving complaints, improving CIR without expanding headcount; (ii)

Credit quality: big-data and AI-driven credit-scoring models extend lending capacity to

segments without traditional credit histories (Vives, 2019); (iii) Service ecosystem:

generative AI integrated into chatbots, automated financial advisory, and personalised

507