Page 504 - ISC PROCEEDINGS 21.4

P. 504

Resource-Based View (Barney, 1991) and Digital Business Strategy literature (Bharadwaj

et al., 2013) predict that heterogeneous resource endowments - particularly in digital

infrastructure and data capabilities - produce persistently differentiated competitive

positions, justifying a cluster-based rather than continuous-scale analytical approach.

Empirically, the classification reflects the structural segmentation observable in Vietnam’s

banking sector: state ownership (C1) creates fundamentally different investment

incentive structures, capital allocation mechanisms, and performance mandates relative

to private banks (C2–C4); within private banks, business model orientation (enterprise

lending vs. retail mass market vs. small institution) drives systematically different digital

investment priorities and capability profiles. This typology is consistent with the

segmentation adopted in the SBV’s own regulatory and supervisory classifications,

enhancing its policy relevance. A key limitation is that cluster assignment is theory-guided

rather than data-driven (e.g., k-means clustering), which may introduce subjectivity. To

mitigate this, all cluster boundaries are anchored to publicly verifiable thresholds (state

ownership status; IT expenditure intensity ≥18% vs. below), reducing discretionary

classification. Future research employing latent class or hierarchical cluster analysis could

provide a more fully data-driven validation of this typology.

While data-driven clustering methods such as k-means or hierarchical clustering

could be applied, they require fully standardised and continuous input variables, which

are not consistently available in the Vietnamese banking context due to heterogeneous

disclosure practices. The threshold-based classification adopted in this study ensures

transparency, replicability, and policy relevance, as all classification criteria are anchored

in publicly observable indicators. The full distribution of 27 listed banks across the four

clusters is as follows: C1 - 4 state-owned banks (BIDV, CTG, VCB, Agribank); C2 - 6

enterprise-oriented banks (TCB, MBB, VPB, MSB, SSB, LPB); C3 - 8 retail-oriented banks

(ACB, STB, VIB, TPB, HDB, EIB, BVB, KLB); C4 - 9 small and medium-sized banks (NVB, ABB,

SGB, BAB, PGB, VBB, BID, NAB, OCB and peers). This distribution is consistent with

publicly available listings on HOSE and HNX as of end-2024.

3. Results and discussion

3.1. Digital infrastructure investment: scale, structure, and development trajectory

Vietnam’s banking sector significantly increased digital infrastructure investment

over the study period. IT expenditure as a share of operating costs, which stood at 5–7%

before 2020, reached 14.85% by 2024, equivalent to approximately VND 32,437 billion

system-wide (MIC, 2018–2024). This level approaches the 15–20% international

benchmark applied by digital-first banks such as DBS (Singapore) and KakaoBank (South

Korea) (World Bank, 2022; Frost, 2020).

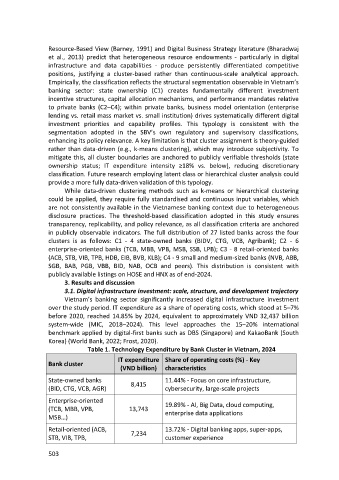

Table 1. Technology Expenditure by Bank Cluster in Vietnam, 2024

IT expenditure Share of operating costs (%) - Key

Bank cluster

(VND billion) characteristics

State-owned banks 8,415 11.44% - Focus on core infrastructure,

(BID, CTG, VCB, AGR) cybersecurity, large-scale projects

Enterprise-oriented 19.89% - AI, Big Data, cloud computing,

(TCB, MBB, VPB, 13,743 enterprise data applications

MSB…)

Retail-oriented (ACB, 13.72% - Digital banking apps, super-apps,

STB, VIB, TPB, 7,234 customer experience

503