Page 792 - ISC PROCEEDINGS 21.4

P. 792

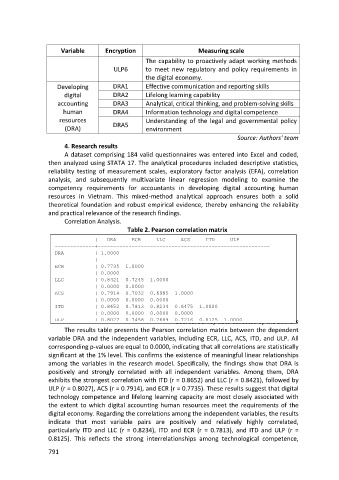

Variable Encryption Measuring scale

The capability to proactively adapt working methods

ULP6 to meet new regulatory and policy requirements in

the digital economy.

Developing DRA1 Effective communication and reporting skills

digital DRA2 Lifelong learning capability

accounting DRA3 Analytical, critical thinking, and problem-solving skills

human DRA4 Information technology and digital competence

resources Understanding of the legal and governmental policy

(DRA) DRA5 environment

Source: Authors' team

4. Research results

A dataset comprising 184 valid questionnaires was entered into Excel and coded,

then analyzed using STATA 17. The analytical procedures included descriptive statistics,

reliability testing of measurement scales, exploratory factor analysis (EFA), correlation

analysis, and subsequently multivariate linear regression modeling to examine the

competency requirements for accountants in developing digital accounting human

resources in Vietnam. This mixed-method analytical approach ensures both a solid

theoretical foundation and robust empirical evidence, thereby enhancing the reliability

and practical relevance of the research findings.

Correlation Analysis.

Table 2. Pearson correlation matrix

| DRA ECR LLC ACS ITD ULP

-------------+--------------------------------------------------------

DRA | 1.0000

|

ECR | 0.7735 1.0000

| 0.0000

LLC | 0.8421 0.7245 1.0000

| 0.0000 0.0000

ACS | 0.7914 0.7032 0.6985 1.0000

| 0.0000 0.0000 0.0000

ITD | 0.8652 0.7813 0.8234 0.6475 1.0000

| 0.0000 0.0000 0.0000 0.0000

Source: Survey data collected by the authors

ULP | 0.8027 0.7458 0.7689 0.7216 0.8125 1.0000

The results table presents the Pearson correlation matrix between the dependent

variable DRA and the independent variables, including ECR, LLC, ACS, ITD, and ULP. All

corresponding p-values are equal to 0.0000, indicating that all correlations are statistically

significant at the 1% level. This confirms the existence of meaningful linear relationships

among the variables in the research model. Specifically, the findings show that DRA is

positively and strongly correlated with all independent variables. Among them, DRA

exhibits the strongest correlation with ITD (r = 0.8652) and LLC (r = 0.8421), followed by

ULP (r = 0.8027), ACS (r = 0.7914), and ECR (r = 0.7735). These results suggest that digital

technology competence and lifelong learning capacity are most closely associated with

the extent to which digital accounting human resources meet the requirements of the

digital economy. Regarding the correlations among the independent variables, the results

indicate that most variable pairs are positively and relatively highly correlated,

particularly ITD and LLC (r = 0.8234), ITD and ECR (r = 0.7813), and ITD and ULP (r =

0.8125). This reflects the strong interrelationships among technological competence,

791