Page 482 - ISC PROCEEDINGS 21.4

P. 482

4.3. Transformer & attention-based generators

Transformer and attention-based generators use self-attention to capture long-

range dependencies and cross-series interactions, improving reproduction of long-

memory effects, cross-asset correlations, and structural regime shifts when trained on

sufficiently long windows; examples include transformer-augmented GANs and hybrid

diffusion/attention frameworks, which typically deliver stronger long-horizon fidelity at

the cost of higher compute, larger data requirements, and careful regularization to avoid

overfitting. where the Transformers serve multiple generative roles in financial data

synthesis, from autoregressive order generators to attention modules inside GANs and

diffusion frameworks like MarketGPT (Wheeler, A. & Varner, J. D., 2024), TTS-GAN (Li, X.

et al., 2022), BankGAN (Mehri, H. et al., 2024), TF-CoDiT(Zhang, F. et al., 2025).

4.4. Privacy-focused variants

Privacy-focused Financial GANs integrate differential privacy, federated learning, or

constraint-aware discriminators to limit disclosure while producing useful synthetic data

for loan-default modeling, fraud detection, audits, and cross-institutional sharing; these

variants, NVF-DPGAN(Zhang, Y. et al., 2026), Fed-DPSDG-WGAN (Ramachandra, P. &

Vaithiyanathan, S., 2025), enable measurable privacy–utility tradeoffs but require careful

tuning and often additional techniques (e.g., tail-augmentation or post-processing) to

preserve extreme events and regulatory-relevant risk metrics.

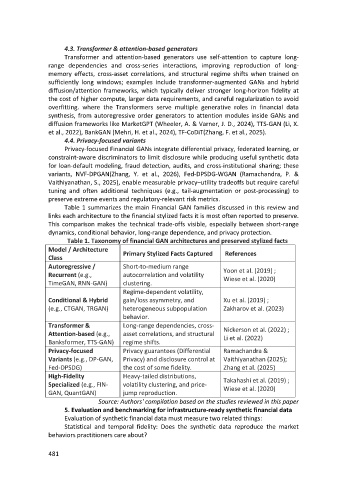

Table 1 summarizes the main Financial GAN families discussed in this review and

links each architecture to the financial stylized facts it is most often reported to preserve.

This comparison makes the technical trade-offs visible, especially between short-range

dynamics, conditional behavior, long-range dependence, and privacy protection.

Table 1. Taxonomy of financial GAN architectures and preserved stylized facts

Model / Architecture Primary Stylized Facts Captured References

Class

Autoregressive / Short-to-medium range Yoon et al. (2019) ;

Recurrent (e.g., autocorrelation and volatility

TimeGAN, RNN-GAN) clustering. Wiese et al. (2020)

Regime-dependent volatility,

Conditional & Hybrid gain/loss asymmetry, and Xu et al. (2019) ;

(e.g., CTGAN, TRGAN) heterogeneous subpopulation Zakharov et al. (2023)

behavior.

Transformer & Long-range dependencies, cross- Nickerson et al. (2022) ;

Attention-based (e.g., asset correlations, and structural Li et al. (2022)

Banksformer, TTS-GAN) regime shifts.

Privacy-focused Privacy guarantees (Differential Ramachandra &

Variants (e.g., DP-GAN, Privacy) and disclosure control at Vaithiyanathan (2025);

Fed-DPSDG) the cost of some fidelity. Zhang et al. (2025)

High-Fidelity Heavy-tailed distributions, Takahashi et al. (2019) ;

Specialized (e.g., FIN- volatility clustering, and price- Wiese et al. (2020)

GAN, QuantGAN) jump reproduction.

Source: Authors' compilation based on the studies reviewed in this paper

5. Evaluation and benchmarking for infrastructure-ready synthetic financial data

Evaluation of synthetic financial data must measure two related things:

Statistical and temporal fidelity: Does the synthetic data reproduce the market

behaviors practitioners care about?

481